Academic Research in Economics & Markets

FinPredict is an independent research platform exploring the intersection of macroeconomics, financial markets, and quantitative analysis. The research published here is intended for academic and educational purposes — examining how economic forces, market structure, and investor behavior interact to drive asset prices over time.

All analysis is generated and reviewed computationally, drawing on publicly available market data, economic indicators, and academic methodologies. Nothing published here constitutes financial advice or an investment recommendation.

Research Areas

Fundamental Analysis

Examination of company financial statements — revenue growth, earnings quality, return on equity, free cash flow, and balance sheet health — to assess intrinsic value and identify momentum in underlying business performance.

Technical Analysis

Application of price-based indicators including moving averages (EMA / DEMA / TEMA), Keltner Channels, Donchian Channels, RSI, and Bollinger Bands to identify mean-reversion and trend-reversal signals across equity and ETF markets.

Sentiment Analysis

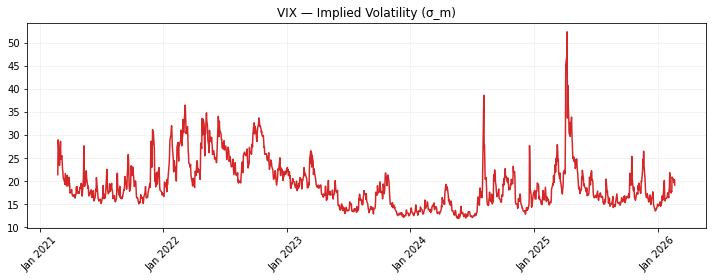

Study of market-wide sentiment proxies — including the VIX volatility index, credit spreads, consumer sentiment surveys, and RSI-based sector momentum — as leading or coincident indicators of risk appetite and market turning points.

Macroeconomic Forces

Tracking of the broad economic backdrop through GDP, inflation (CPI, breakeven rates), labor market data, Federal Reserve policy (Fed Funds rate, balance sheet), treasury yield curves, credit conditions (HY/IG OAS, NFCI), and monetary aggregates (M2).

Regime Classification

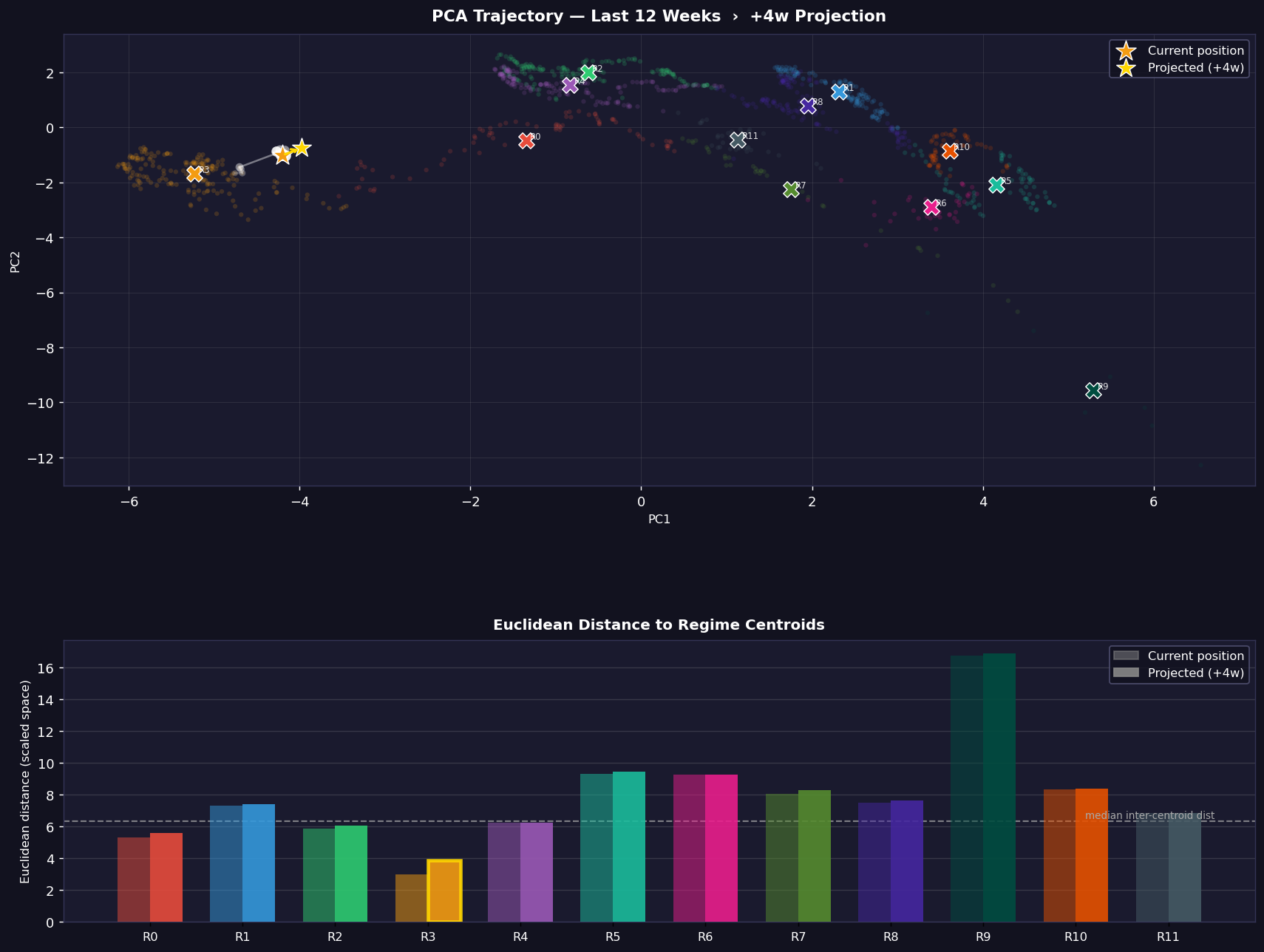

Unsupervised machine learning (K-Means clustering) applied to weekly macroeconomic data to identify distinct economic regimes — periods characterized by coherent combinations of growth, inflation, credit stress, and monetary policy — and to understand how asset behavior differs across regimes.

Simulation & Forecasting

Geometric Brownian Motion and Monte Carlo methods for modeling stochastic price paths, estimating distributional outcomes, and stress-testing portfolios under different regime assumptions.